Personal Contract Purchase (PCP) Explained

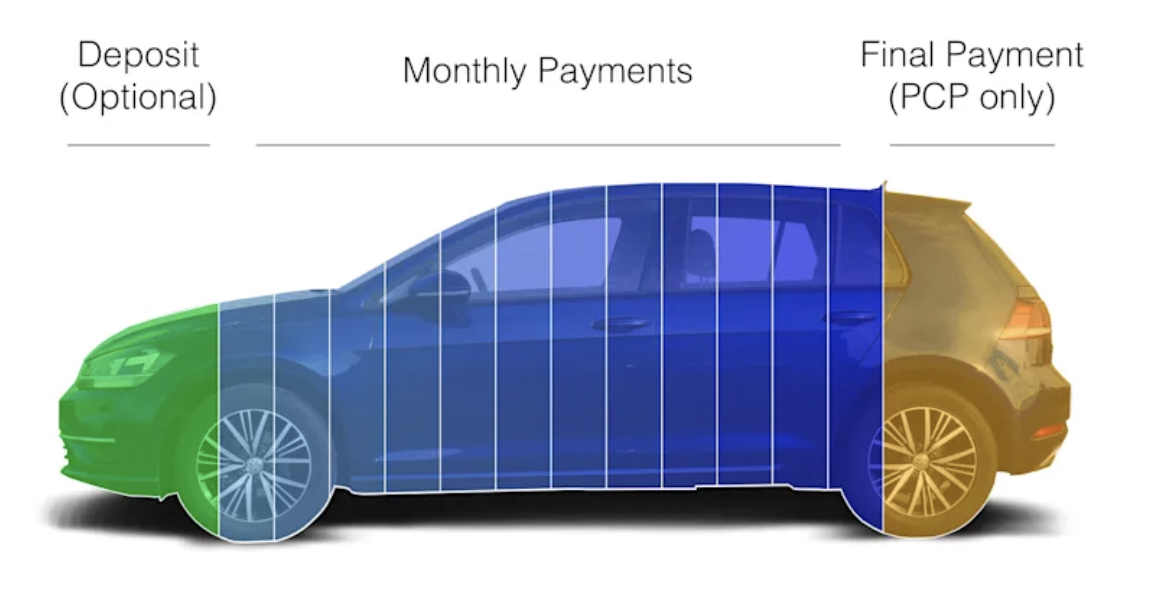

Similar to Hire Purchase, a Personal Contract Purchase allows you to spread the cost of a car over a period of time to match your budget, the rate of interest is fixed and regular payments are made. The difference with a Personal Contract Purchase is that a portion of the borrowing is deferred until the final payment.

The amount of the final payment is based on the future value of the vehicle, taking into consideration make, model and the maximum mileage agreed at the start of the agreement.

This final payment is often referred to as the Guaranteed Future Value.

Because part of the money borrowed is deferred until the end of the agreement your monthly payments will be lower but you will pay more interest overall. This means you could drive a newer or better vehicle than you thought for your monthly budget.

When you get to the end of the agreement (up to 48 months) you have three distinct options:

- Pay the final payment and option to purchase fee and you own the vehicle.

- Part exchange the vehicle for a different one. If the value of the car is more than the amount of the final payment the extra money is yours.

- Hand the vehicle back to the finance company. If when you come to part exchange the vehicle it is not worth the amount of the final payment or if you no longer want a vehicle, the finance company have guaranteed the vehicle will be worth the amount of your final payment so you can walk away with nothing more to pay. Terms and conditions apply, the mileage and condition of the vehicle will also be taken into consideration.

View cars on PCP

Representative Example for Hire Purchase (HP): Cash price £14,700.00, Annual Interest Rate (fixed) 5.14% p.a., with a representative 9.9% APR, total amount of credit £13,230.00, deposit of £1,470.00, an initial payment of £332.24, followed by 46 monthly payments of £332.24 with a final payment of £332.24, total amount payable is £17,417.52